News

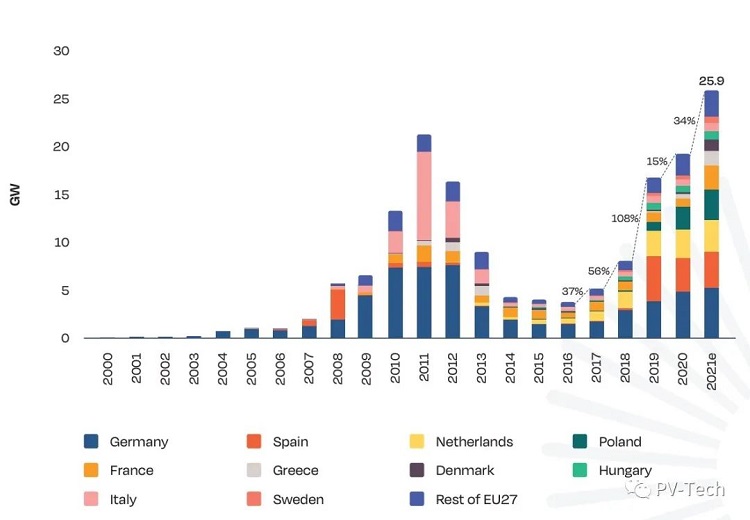

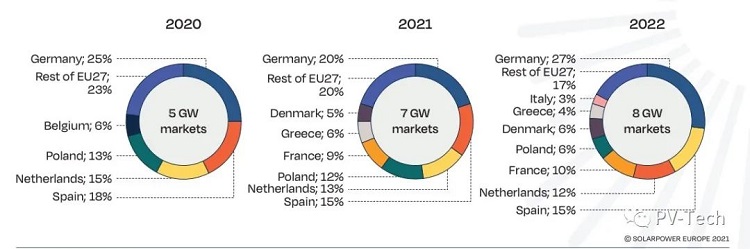

In 2021, about 25.9GW of new solar photovoltaic projects have been connected to the grid in the 27 EU member states, an increase of 34% from the 19.3GW installed capacity of the previous year.

Top 10 EU countries with solar installed capacity in 2021

According to the latest ranking report, the top five EU markets remain unchanged. In the top ten, two new members from Northern Europe (Denmark and Sweden) have replaced two mature photovoltaic markets-Belgium in Central Europe and Portugal in Southern Europe.

Germany: Like last year, Germany will once again become the mainstream solar market in Europe in 2021. The grid-connected capacity was 5.3GW, compared with 4.9GW the previous year. Since the beginning of this century, the European Union’s largest economy has basically maintained its first place. In January 2021, Germany revised the grid connection law.

After the self-use tax is abolished, household and small-scale commercial systems are more attractive for investment, but the larger rooftop self-use system is forced to adopt a bidding scheme, which brings a financial burden. Therefore, for the German market, which will grow approximately 1 GW per year from 2017 to 2020, the expected growth in 2021 is less than half GW (or 8%).

Spain: In Europe, Spain remains at the second place. The expected installed capacity in 2021 is about 3.8GW, a slight increase from the 3.5GW of the previous year. Among the huge projects being developed in Spain, nearly 3GW is based on a power purchase agreement (PPA), which may make this southern European country the world’s largest unsubsidized solar market, but the report also shows that grid restrictions may become The main burden for the rapid development of a large number of solar projects. Most of the 2.9GW solar power plants allocated in the two tenders in 2021 will be completed in 2023.

Netherlands: The Netherlands has an installed capacity of 3.2GW, again occupying the third place, 11% higher than the newly added 2.9GW in 2020. The commercial rooftop market remains the main driver of the Dutch solar market. The share has increased by more than 40%, while the share of the household part supported by the net metering policy has shrunk to about one-third, and the share of ground-based power station systems is still 20%.

Poland: Poland's annual solar installed capacity has increased again, continuing to create surprises for the industry, this time from 2.5GW in 2020 to 3.1GW, an increase of 28%. This means that Poland has maintained its fourth place. Poland is a solar "newcomer", with installed capacity exceeding 1GW for the first time in 2020. In the past few years, the main reasons for the substantial increase in photovoltaic power generation include: self-use plans that are beneficial to production consumers, net metering systems and supplementary household system tax rebate plans, in addition to the decline in value-added tax and income tax.

France: France is still the fifth largest photovoltaic market in the EU. The installed capacity in 2021 is expected to be 2.5GW. This means that on the basis of 0.8GW in 2020, grid-connected solar energy has more than doubled, setting a new record. Over the years, the installed capacity level in France has hovered at 1GW. Long administrative procedures and challenging grid connection procedures have prevented developers from accelerating project development. This level can be said to be a breakthrough for France.

Greece: Greece’s annual photovoltaic development has more than tripled, setting a record of 1.6GW in 2021, a significant increase from 0.5GW in 2020. The annual installed capacity exceeding the GW level for the first time indicates that Greece ranks sixth in the EU solar market. This boom is mainly driven by small ground photovoltaic projects below 500kW. The government has recently postponed the online tariff policy for these projects until the end of 2022.

Denmark: In 2021, none of the top ten solar energy markets in the EU will grow at a rate comparable to that of Denmark. The newly-rising EU Solar Star’s annual installed capacity has increased from only 0.2GW in 2020 to 1.2GW, a 6-fold increase. The scale of gigawatt projects is almost entirely realized through unsubsidized large-scale ground photovoltaic power plants, which are used to supply power to corporate buyers.

Italy: The 110% tax incentive supported by the COVID-19 Recovery Fund has triggered greater demand for household and energy storage projects, but serious licensing issues and disappointing solar tenders have resulted in the largest and sunniest economy in Europe The new installed capacity of one of the entities is only 0.8GW.

Hungary: The strong interest in small ground-based power station systems and household and commercial rooftop projects below 50kW have made Hungary's solar performance this year very good. In 2021, the annual solar grid-connected capacity will increase to 0.7GW.

Sweden: The latest country to enter the top ten is Sweden. Sweden’s tax incentives and subsidies continue to drive demand growth. As activities in the field of solar PPA become more and more active, in 2021, the installed capacity will reach a record 0.7GW.

2022-2025, growth prospects are promising

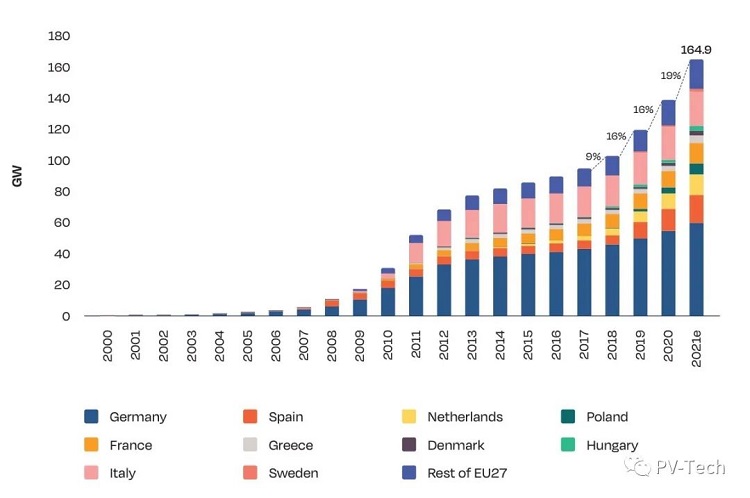

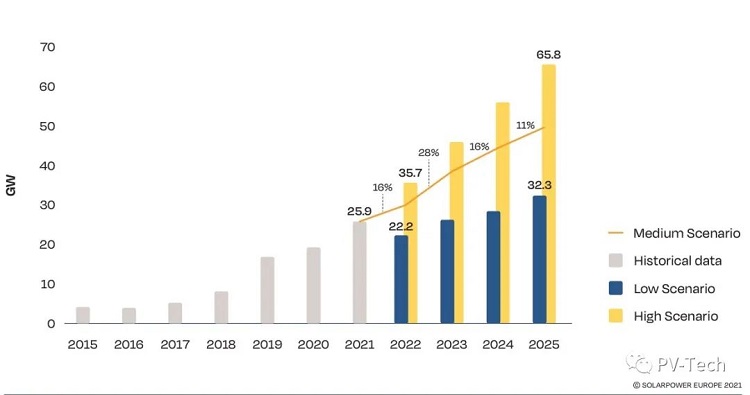

According to the report's mid-term plan, the next four years to 2025 will be characterized by further strong growth. SPE predicts that by 2030, the EU's total solar power generation will increase from the current 165GW to 672GW.

However, judging from the 16% annual growth rate, European solar energy will reach the 30GW threshold for the first time in 2022, becoming another record year.

With prices returning to normal, the new plan for large-scale solar projects in Germany will be launched in 2023, and the annual market size will reach 10GW for the first time. We expect the EU will see a 28% increase to 38.5GW.

In the next two years, the growth rate will become more moderate-16% in 2024 and 11% in 2025. Nonetheless, this is enough to make the annual solar development more than 40GW-44.6GW in 2024, 2025 49.7GW per year, which is close to the level of 50GW.

However, judging from the 16% annual growth rate, European solar energy will reach the 30GW threshold for the first time in 2022, becoming another record year.

With prices returning to normal, the new plan for large-scale solar projects in Germany will be launched in 2023, and the annual market size will reach 10GW for the first time. We expect the EU will see a 28% increase to 38.5GW.

1499 Zhenxing Road, Shushan District, Hefei,China

+86 158-5821-3997

+86-0551-6565-2651

Friendly Links :

Copyright © 2016 Bluesun Solar Co.,Ltd All Rights Reserved. 皖ICP备2021006055号-2